A Special Situation with a 35% IRR

Quick Pitch

High quality business with recurring revenues and 90% gross margins

Trading at 4.5x 2025 EBITDA

To be acquired at a 17% higher share price by mid 2025

Galaxy Gaming (GLXZ)

Galaxy Gaming is a global provider of proprietary casino table games, systems, and iGaming content. The company develops, licenses, and sells table games, side bets, and jackpot systems to land-based casinos as well as content to iGaming operators for online casino platforms.

The business is divided into two segments.

GG Core- Their ‘physical world’ segment where they license their products to casinos, racinos, and cruise ships and to providers of gaming devices.

Some of their proprietary table games are 21+3, Lucky Ladies, and Bonus Craps. The casinos use these games alongside other games like Blackjack.

Bettors enjoy these games as they add the potential for higher payouts and casinos like them as they have a better edge than on other games. For example, on Blackjack, the house has between a 0.5% and a 2% edge compared to between a 5% and 20% edge on GLXZ’s games.

Based on their Q3 earnings, about 68% of the revenue came from this segment

GG Digital- this segment focuses on licensing their table games to online casino platforms and Igaming operators.

Based on their Q3 earnings, 32% of their revenue came from this segment.

Most of their revenue is recurring, as they get paid monthly. Depending on the contract, payments are either a flat rate or based on the actual revenue or usage generated from the game. In 2023, they entered into a perpetual license arrangement with a large customer in which the customer paid upfront to have perpetual rights to the gaming systems. In Q3 about 11.9% of their revenue came from the perpetual license arrangements with the rest coming from recurring license revenue.

As this is a quick pitch I’m not going to go into detail about the business but if you’re interested in learning more the former CEO did a business breakdown with MicroCapClub and did a podcast with Planet Microcap.

Acquisition

On July 18, it was announced that Evolution ($EVO.ST) would acquire Galaxy Gaming at $3.20 per share. (which implies a $85 million market cap) which was a 124% premium to galaxy gaming’s share price at the time.

GLXZ shares instantly jumped to $2.80 a share but have continued to hover there till now where is slightly dropped to $2.73 a share.

The acquisition has been approved by Galaxy Gaming shareholders and is meant to close mid 2025 which means assuming the deal closes in July you would get about a 35% IRR.

Even if you assume the acquisition gets delayed all the way until October you’ll still get a 21% IRR.

What happens if the acquisitions doesn’t go through?

If the acquisition doesn’t go through you’ll be left holding shares of Galaxy gaming but I don’t think that it’s necessarily a bad thing.

If the deal falls through GLXZ gets $5.2 million which would increase their cash pile from $17.9 million to $23.1 million.

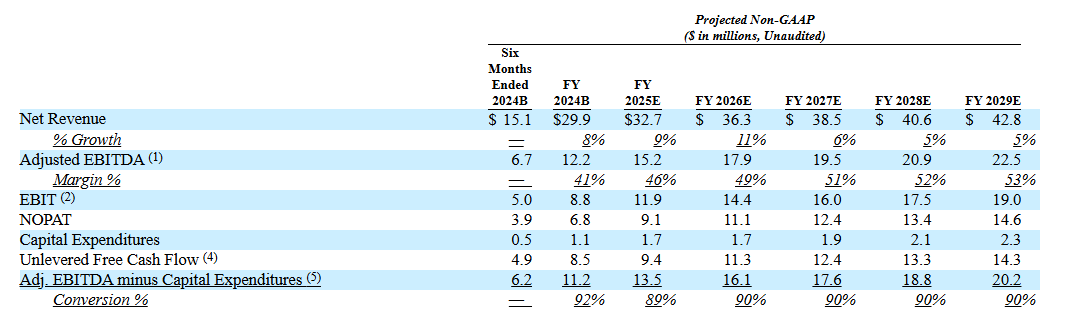

Additionally, in an 8-K filed on November 1, the company outlined projected earnings through 2029.

Assuming they’re able to reach these projections GLXZ is currently trading at 4.5x 2025 EBITDA while expecting EBITDA to grow at a 10.7% CAGR till 2029.

Based on the acquisition price, Evolution is buying Galaxy Gaming at just 5.2x 2025 EBITDA which for a asset light business that is growing EBITDA at 10% a year seems like a bargain to me.

Debt

If you look at GLXZ financial statements you would instantly find one massive red flag which is their long term debt. As of September 30 they had $53.8 million in long term debt.

The story of why they took on the debt is very interesting. The Nevada Gaming Commission threatened to reject the company’s license application because of the founder’s past. So, the company had to buy out the founder’s shares, who owned 60% of the total shares. (in the business breakdown they talk more about this)

Galaxy Gaming took $60 million in financing from Fortress, maturing in November 2026, with an interest rate of approximately 13%, based on the 3-month SOFR rate plus a fixed margin.

Because of this debt, they are paying about $7 million in annual interest payments which is killing their bottom line.

What I find weird is the company has $17 million in cash which they could use to pay off some debt to decrease the interest payments.

The CFO on May 23 made a video responding to some investor questions and this was his explanation for not paying off part of the debt.

The first question asked why we keep so much cash on our balance sheet when we could use some of it to pay down the Fortress debt.

that question is a fair one as there is currently about an 800 basis point spread between what we earn on our cash and what we pay on our debt however the number one concern that we hear from investors is that we might default on our debt with the result that creditors would take over the company in bankruptcy we think that's unlikely but the best way to prevent it is to pay interest in on time and we are keeping the cash on hand in order to make sure that we can do that even if economic conditions worsen significantly.

The cash we had at March 31 around 17.5 million represents more than 2 years of interest and mandatory principal payments we could take 10 million and make a partial payment on the Note but then the remaining cash would only cover a year's worth of interest at current interest rates and would not cover the minimum amortization so we view the negative interest on the high cash balances as essentially an insurance premium against the failure to pay interest and principal when due.

I personally think that’s a pretty weak answer and it’s possible the company did too as a new CFO took over just 5 days after the video was created.

The new CFO is Steve Kopjo, and his LinkedIn profile indicates that he has experience in M&A and debt restructuring, which I believe GLXZ desperately needs. If the acquisition doesn’t go through, he should have $22 million to work with.

Risk

The only risk I see with the deal not going through would be regulatory risks as Pitching Value pointed out to me is that Evolution is quite monopolistic.

As for business risks, if the deal doesn’t go through, they could mismanage the debt, completely miss their projections, or encounter other unforeseen business issues.

Disclosure- I’m currently long shares of Galaxy Gaming with a average price of $2.73

Happy Holidays!

I also created a reader survey to know what kind of articles you guys prefer so if you can fill it out it would greatly appreciated!

The information provided in this write-up is for informational purposes only and should not be considered financial advice. I am not a licensed financial advisor, and this analysis reflects my personal opinions and research. I may own, or plan to purchase, shares in the stock discussed. Do your own due diligence before making any investment decisions, as stock investing carries risks, including the loss of principal. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any financial decisions.

working on christmas thanks!

Do you have any info on any past acquisitions done by Evolution in US ? Would provide some context about chances of approval.