Stock Updates: 5 Previously Profiled Stocks

Updates on a few different stocks

Below are a few brief updates on previously profiled stocks. I didn’t write an update on every stock I wrote up as the first few were very different from my current investment style.

Sun Residential Real Estate Investment Trust

A Nanocap REIT trading at 0.37x P/B with a 8.4% Dividend Yield

About 2 months ago, the Multibagger Monitor (I highly recommend you follow him as he’s a great investor) made a post on X sharing a few interesting ideas and his thoughts about them. For this company he wrote “Tiny cheap REIT with a great dividend, but probably too small and might be impossible to buy”. This immediately caught my attention, so I decided…

Conclusion from write-up - Stock was very cheap trading at less than half of book value with over half its market cap in cash while paying a 8.4 % dividend yield.

Total Return since Write-Up : 135.44%

Since the write-up - $SRES.V announced that they were liquidating both of their properties. The share price has since jumped to 0.105 and the liquidate distribution estimate is 0.111 that will be paid in two parts one in late June and the final one at the end of September.

Kinovo PLC

A Microcap with 99% Recurring Revenue

All numbers in this write-up are in British Pounds unless specified otherwise

Conclusion from write-up- A high quality micro cap that had short term problems after selling a lower margin subsidiary. With 99% recurring revenue and almost all the issues solved it seemed very cheap even with the assumption of little to no revenue growth.

Total Return since Write-up: 32.81%

Since the write-up- On May 12, Kinovo received a takeover bid at 87.5 pence a share. Assuming this goes through the total return since my write-up would be 36.7%.

I think the take-over price is too low and I’d prefer to hold my shares to see how the business performs over the next few years. Paul, not a CFA wrote a great thread about it .

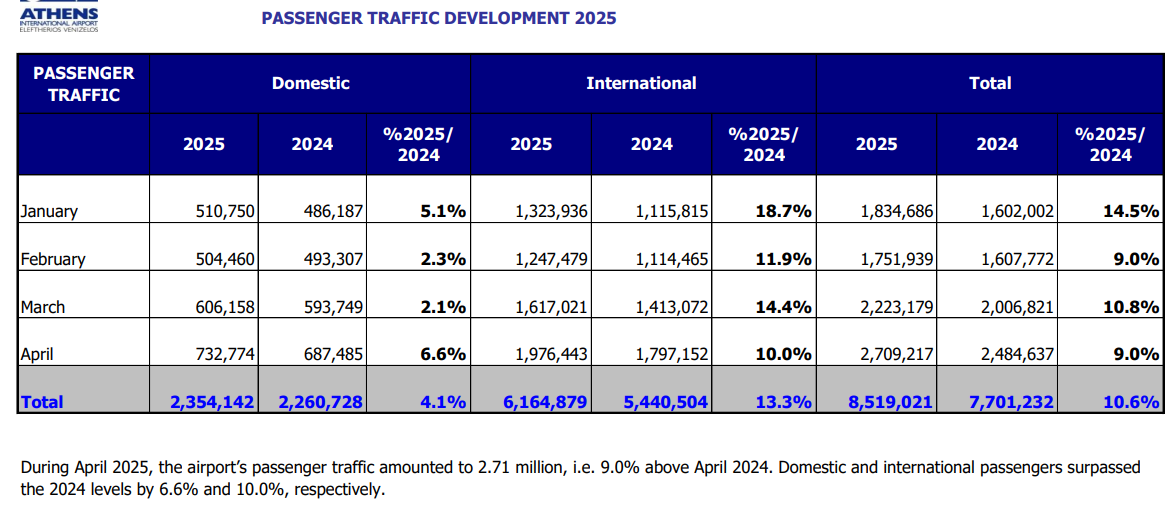

Athens International Airport

Athens International Airport- A True Monopoly

NOTE- All numbers in this write up are in euros unless specified otherwise

Conclusion from write-up- A high quality business trading at a double digit FCF yield. While they were slightly overearning it was quite cheap for such a high quality company that was expecting growth.

Total Return since Write-up : 24.83%

Since write-up- Athens Airport has had great passenger growth in 2025 as they’ve had 10.6% more passengers in 2025 than 2024.

In their Q1 trading update, revenue was up 9% from Q1 2024 to $125 million with air activity revenue up 6.3% and non-air revenues up 17.5%. (It’s important to note that Q1 is their weakest quarter)

Despite the revenue growth, net profit was down 8.1% to €26.2 million. This was expected as they no longer had the air activity carry-forward and faced a higher Grant of Rights Fee, due to increased profitability in 2024.

The company’s scrip dividend program was €235.6 million (€0.78 per share), with €84 million reinvested back into the company at €8.88 per share. The proceeds will be used to develop the a new Apron (North-West Apron) and the designing of the main terminal building. This allows AIA to continue their expansion plan without taking out more debt and allows the company to earn more as the proceeds increase Air Activities capital which the company can earn up to a 15% ROE.

( 9.5 million new shares will start trading on May 16)

Conclusion from write-up- A nanocap with 87% recurring revenue that’s quickly growing revenue using acquisitions trading at 7x FCF. While I thought it was cheap they were diluting too much for my liking and I was waiting to see how the new acquisition would turn out.

Total Return since Write-up: -6.85%

There isn’t really any update since I posted this write-up, as no news or financials have been released. But the stock was already pretty cheap when I wrote it up, and now it’s cheaper. I’m still waiting to see how the acquisition works out and if they keep diluting, but if the stock keeps getting cheaper, I may buy some shares.

Galaxy Gaming

Conclusion from write-up- A interesting merger-arb with a potential 35% IRR. If deal doesn’t go through you got a asset light business with $22 million in cash that is expecting to grow EBITDA at a 10.7% CAGR until 2029 (with a lot of debt)

Total Return since Write-up : 2.18%

One of the things I mentioned in my quick pitch was how they had a lot of cash yet they weren’t paying of any of their long term debt and they had fired their CFO.

The new CFO (Steve Kopjo) has got to work on this by refinancing their debt. They closed a five-year, $45 million secured term loan due 2030. This loan’s interest rate is SOFR plus 3.50%, which is significantly better than their previous interest rate which should save the company $2.8 million annually. While their balance sheet isn’t good, it’s much better than it was before.

I’m thinking of writing another write-up on $GLXZ as the story has changed a bit because the acquisition has likely been delayed to the end of 2025 and the financials of the company have changed quite a bit.

Disclosure - I own shares in $SRES.V, KINO.L, and $GLXZ

The information provided in this write-up is for informational purposes only and should not be considered financial advice. I am not a licensed financial advisor, and this analysis reflects my personal opinions and research. I may own, or plan to purchase, shares in the stock discussed. Do your own due diligence before making any investment decisions, as stock investing carries risks, including the loss of principal. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any financial decisions

Appreciate your work!

Where did you find the galaxy merger being delayed until end of 2025?